RENEW OR SELECT YOUR COVER

RENEW OR SELECT YOUR COVER

RENEW OR SELECT YOUR COVER

Health Insurance

With rising inflation and ever-increasing medical expenses, investing in health insurance has become more imperative now than ever. Your health insurance policy goes a long way in securing your savings and ensuring you can get the best medical treatment money can buy. Health insurance is a contract between an insurance company and a policyholder, wherein the former covers medical costs up to a specific amount known as the sum insured, in exchange for an amount or premium paid by the latter.

A health insurance agreement comprises several clauses pertaining to the type of coverage you are entitled to, the amount the insurer is obligated to pay when you file a claim, and the terms under which an insurer may approve or reject your claim. With medical insurance, you can rest assured that the insurer will bear a significant portion of your medical treatment costs up to the sum insured amount.

Types of Health Insurance Plans

Insurance companies generally classify medical insurance plans into two types – indemnity-based plans and definite plans.

Individual Health Insurance Plans

Health insurance plans covering a single individual are known as individual health insurance plans. As an individual health policyholder, you are the primary and only beneficiary eligible for coverage under the policy. You can utilise the entire sum insured while seeking medical treatment. You cannot transfer or share the benefits provided under this policy with another individual

Family Floater Health Insurance Plans

You can cover all your family members, including yourself, your spouse and your children, under a single health insurance policy known as the family floater plan. In these plans, all insured members must share the sum insured amount. You can file multiple claims per annum and seek treatment simultaneously, if needed, until you exhaust the entire sum insured. Family floater plans are less expensive as compared to individual health insurance policies.

Senior Citizen Health Insurance Plans

Senior Citizens typically need more medical attention and are more likely to file insurance claims than young people. Keeping this in mind, insurance companies offer senior citizen health insurance plans. If you wish to purchase this insurance plan, you may need to undergo a medical check-up at a hospital under the insurer's network, based on which the insurer determines the premium amount and the maximum coverage they can offer.

Group Health Insurance Plans

Many companies provide health insurance benefits to their employees under group health insurance plans. If you are covered under such a policy, the onus of paying the insurance premiums does not fall on you. Your employer sponsors the insurance as one of the perks of being a part of their organisation. However, you will remain eligible for coverage only until you remain employed with the organisation. The employer terminates your group health insurance policy once you leave the company.

Health Insurance Coverage

What is Included Under Health Insurance Plans

A health insurance policy covers the costs of most medical expenses.

The standard coverage included in your health plan is as follows.

In-patient Hospitalisation

Your insurer covers all the costs pertaining to hospitalisation up to the sum insured limit. The commonly covered costs include hospital room rent, surgeon fees, medicines and apparatus used during surgeries, anaesthesia costs, wound dressing and care, and so on. The hospital typically mentions these expenses in the itemised bill.

Pre and Post- Medical Expenses

The expenses pertaining to the treatment for which you are filing a claim are covered under pre and post-hospitalisation expenses. You may need to undergo tests, x-ray screenings, biopsies, etc., before and after your medical treatment. You may also need to go for follow-up consultations, removal of sutures, etc. These costs are covered under your insurance plan.

Day-care Treatments

Some medical conditions may not warrant hospitalisation and can be completed within a few hours. Such treatments are known as day-care treatments. Insurers typically mention the medical conditions against which they cover day-care treatments in the policy document

Organ Donor Expenses

If you need to undergo an organ transplant, the insurance provider covers the hospitalisation costs of your donor too. However, the coverage for organ donors is usually limited, and insurers do not cover ambulance costs or the pre and post-hospitalisation costs associated with donors.

Alternative Treatment Cover

If you feel that allopathy alone is insufficient for your treatment, your health insurance provider covers the costs of alternative therapies. These include Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homeopathy, i.e. AYUSH treatments. By including AYUSH under the scope of coverage, insurers ensure you can get a holistic treatment approach.

Mental Health Cover

Insurers today also cover the costs of mental health treatments under a standard health insurance policy. Thus, you can seek treatment for various mental health conditions, such as anxiety, depression, bipolar disorder, schizophrenia, post-traumatic stress disorder, etc., at network hospitals or file a reimbursement claim.

Routine health check-ups

Your insurance provider covers the cost of routine health check-ups. Most insurers bear health check-up costs once a year and reimburse you up to a specific limit. This coverage allows you to track your health and the changing conditions, detect illnesses in their nascent stage, and begin your medical treatment before it advances significantly.

In-patient Hospitalisation

Your insurer covers all the costs pertaining to hospitalisation up to the sum insured limit. The commonly covered costs include hospital room rent, surgeon fees, medicines and apparatus used during surgeries, anaesthesia costs, wound dressing and care, and so on. The hospital typically mentions these expenses in the itemised bill.

Pre and Post- Medical Expenses

The expenses pertaining to the treatment for which you are filing a claim are covered under pre and post-hospitalisation expenses. You may need to undergo tests, x-ray screenings, biopsies, etc., before and after your medical treatment. You may also need to go for follow-up consultations, removal of sutures, etc. These costs are covered under your insurance plan.

Day-care Treatments

Some medical conditions may not warrant hospitalisation and can be completed within a few hours. Such treatments are known as day-care treatments. Insurers typically mention the medical conditions against which they cover day-care treatments in the policy document

Organ Donor Expenses

If you need to undergo an organ transplant, the insurance provider covers the hospitalisation costs of your donor too. However, the coverage for organ donors is usually limited, and insurers do not cover ambulance costs or the pre and post-hospitalisation costs associated with donors.

Alternative Treatment Cover

If you feel that allopathy alone is insufficient for your treatment, your health insurance provider covers the costs of alternative therapies. These include Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homeopathy, i.e. AYUSH treatments. By including AYUSH under the scope of coverage, insurers ensure you can get a holistic treatment approach.

Mental Health Cover

Insurers today also cover the costs of mental health treatments under a standard health insurance policy. Thus, you can seek treatment for various mental health conditions, such as anxiety, depression, bipolar disorder, schizophrenia, post-traumatic stress disorder, etc., at network hospitals or file a reimbursement claim.

Routine health check-ups

Your insurance provider covers the cost of routine health check-ups. Most insurers bear health check-up costs once a year and reimburse you up to a specific limit. This coverage allows you to track your health and the changing conditions, detect illnesses in their nascent stage, and begin your medical treatment before it advances significantly.

Standard Health Insurance Exclusions

Your insurer lists the various conditions and treatments for which you cannot file a claim in the policy document. These are known as exclusions in medical insurance and typically include the following.

Medical Conditions Attributed to Lifestyle

Insurers are not liable to cover your medical expenses if your condition is caused due to certain lifestyle choices you may have made. For instance, an insurer will not cover the costs of mouth cancer if you smoke or consume tobacco. Similarly, they may not cover the costs of lung diseases or cirrhosis caused by alcoholism.

Voluntary Cosmetic Treatments

You cannot file a claim for voluntary cosmetic treatments such as rhinoplasty, implants, plastic surgery to enhance your features, etc. However, if a medical practitioner recommends a cosmetic procedure due to injuries sustained in an accident or due to criminal activities (as in the case of acid victims), the insurer may cover the costs.

Fertility Treatment & Pregnancy Termination

While insurers today offer a maternity add-on cover, they do not cover you for costs associated with fertility treatments and voluntary termination of pregnancies. Thus if you wish to undergo in-vitro fertilisation (IVF) treatment to conceive a baby or if you choose to terminate a no-risk pregnancy, insurers are not liable to cover the costs of the same. If, however, your pregnancy puts your life at risk, you may be eligible for coverage under your medical insurance plan.

Medical Conditions Attributed to Lifestyle

Insurers are not liable to cover your medical expenses if your condition is caused due to certain lifestyle choices you may have made. For instance, an insurer will not cover the costs of mouth cancer if you smoke or consume tobacco. Similarly, they may not cover the costs of lung diseases or cirrhosis caused by alcoholism.

Voluntary Cosmetic Treatments

You cannot file a claim for voluntary cosmetic treatments such as rhinoplasty, implants, plastic surgery to enhance your features, etc. However, if a medical practitioner recommends a cosmetic procedure due to injuries sustained in an accident or due to criminal activities (as in the case of acid victims), the insurer may cover the costs.

Fertility Treatment & Pregnancy Termination

While insurers today offer a maternity add-on cover, they do not cover you for costs associated with fertility treatments and voluntary termination of pregnancies. Thus if you wish to undergo in-vitro fertilisation (IVF) treatment to conceive a baby or if you choose to terminate a no-risk pregnancy, insurers are not liable to cover the costs of the same. If, however, your pregnancy puts your life at risk, you may be eligible for coverage under your medical insurance plan.

Health Insurance – Key Feature

Some salient features of general medical insurance plans include the following.

Cashless Treatment

Cashless treatment means that you can seek admission into a hospital without making any payment. The caveat to avail cashless treatment is simple – you must ensure you seek treatment in a hospital under the insurer's network, from those mentioned in the health insurance policy document. You must inform the insurer about your chosen network hospital. The insurer then reaches out to the hospital administration to complete the payment formalities.

Reimbursement Facility

Many health insurance plans come with a complimentary health check-up facility. It simply means that you get a routine health check-up, and the insurer will bear the costs of the same. The insurer covers the costs up to a predetermined amount per the policy terms. They also mention the number of times you can obtain this complimentary check-up, which is typically once or twice a year, based on your chosen policy type.

Customisable Coverage

You can customise your policy to your liking with the help of additional riders. You can choose from an extensive range of add-on riders to maximise your coverage. You must pay a separate fee for each additional rider you opt for, over and above the general premium amount. Standard add-on riders you can get include ambulance coverage, maternity cover, room rent waiver, personal accident rider, etc.

No-Claims Bonus

A no-claims bonus is a reward insurers offer you for not filing claims in a given policy year. This facility enables you to enhance your sums insured without paying an additional premium. Typically, insurers enhance your sum insured by a specific percentage for every claim-free year, up to five consecutive years. Thus, if you do not file insurance claims for five continuous years, your insurer may increase your sum insured by 50% at no extra cost.

E-opinion

Most insurance providers today offer an e-opinion facility under health insurance plans. This feature entitles you to seek a second opinion online with a different medical practitioner to ensure you have the correct diagnosis and treatment plan. You can typically seek an e-opinion with a hospital under the insurer's network, and your insurance provider bears the cost of the same up to a predetermined amount.

Sum Insured Refill

Sum insured refill is a facility that enables you to reset your sum insured amount in a given policy year after you have utilised it. You can reset your sum insured amount partially or wholly. Insurers typically offer this facility with family floater plans that cover several individuals under a single sum insured. You can file multiple or simultaneous claims for various insured parties during a policy year by resetting the sum insured.

Complimentary Health Check-up

Many health insurance plans come with a complimentary health check-up facility. It simply means that you get a routine health check-up, and the insurer will bear the costs of the same. The insurer covers the costs up to a predetermined amount per the policy terms. They also mention the number of times you can obtain this complimentary check-up, which is typically once or twice a year, based on your chosen policy type.

Policy Modifications

Insurers allow you to assess and modify your policy every year. You can enhance or reduce your coverage based on your changing needs. For instance, you can add new members to an existing policy or suspend coverage for others. You can also enhance your sums insured, add or remove riders, adjust the deductible or co-payment amounts, etc. However, you can modify your policy only once a year at the time of renewal.

Health Insurance Benefits

You can enjoy the following benefits with your health insurance plan.

Convenient Onboarding

You can now buy health insurance policies online without extensive paperwork. You can research various health plans online and shortlist your preferred insurance policy. Many insurers today allow you to purchase health insurance through mobile applications. Alternatively, you can buy insurance the conventional way, i.e., through insurance agents or brokers.

Savings Protection

Expensive medical treatments can put a severe dent in your savings. However, a health insurance policy ensures that your savings remain intact. You can simply encash your health insurance policy, and the insurer will bear the costs of medical treatment up to the sum insured amount. Thus by paying a small yearly premium, you can safeguard your savings.

Family Security

You can ensure medical coverage for all family members with medical insurance. You can buy individual health insurance plans for your family members or purchase a single family-floater policy covering all members of your immediate family. Also, insurers provide an add-on death benefit cover with specific policies. This cover ensures your family’s financial security in your absence.

Wide Coverage

Your health insurance policy covers you against a range of physical and mental health conditions. Whether you need treatment against common viruses or critical illnesses like cancer, kidney failure, cardiovascular diseases, etc., your policy covers the costs up to the sum insured. You can also seek alternative treatments like Ayurveda, Yoga, Naturopathy, etc., under health insurance

Cost-effective Investment

Of all the investments you make in a year, buying a health insurance policy is the most cost-effective investment. You typically have to pay a small sum in exchange for coverage ranging into several lakhs, sometimes a few crores. For instance, your insurer may only charge you ₹25,000 per annum to cover you against medical costs ranging from ₹5 lakhs to ₹10 lakhs per annum.

Seamless Claim Settlement

Most insurers ensure you do not have to go through obstacles or hurdles in getting your claims settled. As long as you provide the original medical bills and copies of your medical diagnosis and other essential records, they will settle your claims seamlessly. Insurers generally settle medical insurance claims within three weeks or 21 business days.

Reduced Tax Outgo

Investing in a health insurance policy also allows you to reduce your tax outgo significantly. You can save anywhere from ₹25,000 to ₹100,000 per annum in tax payment under Section 80 D. Moreover, if you are bearing the costs of medical treatments for dependents with specific illnesses, or physical disabilities, you can reduce your tax outgo even further.

Peace Of Mind

Health insurance gives you the confidence to seek treatment at any hour, at any hospital, without having to worry about costs. It gives you a sense of mental and financial security and peace of mind, thus preparing you to face any medical emergency. All you need to do is inform your insurer about your intention to file a claim, and you can begin seeking treatment.

Important Health Insurance

Your health insurance policy comprises a series of standard terms and jargon that insurers repeatedly mention in the policy document. It is thus essential that you familiarise yourself these terminologies. The standard terms you should know include the following.

Waiting Period

In health insurance, the waiting period refers to the amount of time during which you cannot file an insurance claim. The waiting period ranges from three to six months for standard health insurance policies. It can go up to 24 to 48 months for critical illness policies or coverage against pre-existing diseases. However, insurers waive the waiting period in case you need hospitalisation in the event of an accident.

Deductibles

Some insurance policies come with a deductible clause, under which you, as the policyholder, are obligated to bear the medical costs up to a certain amount known as the deductible. The insurer covers the medical costs exceeding the deductible. This deductible is usually mentioned as a percentage or a fixed sum. If the medical cost is lower than the deductible amount, the insurer is not liable to bear the costs. Selecting a medical insurance plan with a deductible can reduce your premium costs.

Co-payment

Co-payment refers to a specific portion of the claim amount you, as the policyholder, must pay out of your pockets. The insurance company covers the remaining costs up to the sum insured. With co-payment, you agree to share or co-pay the costs of the medical expenses up to a predetermined amount of the total admissible claims amount. Like with deductibles, opting for the co-payment clause can reduce your premium costs significantly.

Network Hospitals

Insurance companies usually tie up with various hospitals countrywide, where you can seek cashless treatment. These hospitals are registered under the insurer's network and are thus known as network hospitals. If you seek treatment at a network hospital, you do not have to worry about making cash payments upfront. You only need to inform the insurer about where you intend to seek treatment, and the insurer contacts the hospital and completes the payment formalities.

No-Claim Bonus

Insurers reward you for not filing claims during a given policy year. This reward is known as a no-claims bonus, under which the insurer increases your sum insured amount without increasing your premium payment. With the no-claims bonus, you can enhance your sum insured amount by 10% for every claim-free year, with a maximum increase of 50% for five consecutive claim-free years.

Pre & Post Hospitalisation Costs

Before being hospitalised, you may need to undergo various medical tests, X-rays, screenings, etc. Similarly, your doctor may recommend follow-up tests and procedures (such as removal of stitches, biopsies, etc.) after you are discharged from the hospital. Such expenses are part of your medical treatment plan, which is why the insurer covers them under pre and post-hospitalisation costs.

Grace Period

Insurance companies recognise that sometimes you may be busy and unable to renew your health insurance plan by the renewal date. This is why they offer a 15 to 30 days grace period during which you can renew your insurance policy. The grace period is simply an extended period the insurer provides to allow you to renew the policy without losing its benefits. If you fail to renew your insurance plan during this time, the insurer terminates your policy.

Portability

If you wish to transfer your existing health insurance plan to a different insurance company, you can do so with the portability facility. With portability, you can transfer the benefits accrued from your existing health insurance company to the new insurer. Some benefits you can port include the no-claims bonus, the completed waiting period, etc. You can port your policy to a new insurer within 45 to 60 days before the policy renewal date.

Claim Settlement Ratio

A claim settlement ratio refers to the numeric value, usually expressed as a percentage. It gives you an insight into how fast and how many claims an insurer approves or rejects each year. This ratio represents an insurance company's ability and speed while settling claims. You can assess an insurer's claim settlement ratio on the Insurance Regulatory and Development Authority of India (IRDAI) website before shortlisting one with a high claim settlement ratio.

Outpatient Department Treatment

Insurers require you to be hospitalised overnight or for at least 24 hours to approve your medical insurance claims. However, they cover the costs of specific treatments for which you may not need overnight hospitalisation. Such treatments are known as outpatient department (OPD) treatments. Common examples of OPD Treatments include chemotherapy, dialysis, dental treatments, etc.

Health Insurance Add-on Riders

You can customise your health insurance policy with an array of additional riders per your needs. The insurer levies a separate charge for each additional rider you choose. The standard riders you can add to your include policy include the following.

Health InsuranceTax Benefits

You can enjoy several tax reduction benefits on your health insurance investments for yourself, your spouse, your children, and your parents. Under Section 80D of the Income Tax Act of India, 1961, you can claim deductions ranging from ₹25,000 to ₹100,000 per annum, based on the age of the insured parties.

Deductions up to

₹25,000.

You can enjoy annual deductions of up to ₹25,000 for purchasing health insurance plans for yourself, your spouse and your family. You must ensure that all insured parties, including you as the policy buyer, are under the age of 60 years to claim the deductions. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹50,000.

Besides paying the insurance premiums for your immediate family, you can also purchase a medical insurance plan for your parents and get an additional annual tax deduction of ₹25,000. Doing so enables you to obtain annual tax deductions of ₹50,000. Once again, all insured parties must be under 60 years for you to qualify for these deductions. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹75,000.

Besides paying the insurance premiums for your immediate family, you can also purchase a medical insurance plan for your parents and get an additional annual tax deduction of ₹25,000. Doing so enables you to obtain annual tax deductions of ₹50,000. Once again, all insured parties must be under 60 years for you to qualify for these deductions. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹1,00,000.

As the policy buyer, if you are above 60 years of age and still purchasing health insurance plans for your immediate family members (up to 60 years) and senior citizen parents, you can claim annual tax deductions of up to ₹100,000. The deduction is categorised as ₹50,000 for policies purchased for yourself and your kin and another ₹50,000 for policies purchased for your senior citizen parents. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹25,000.

You can enjoy annual deductions of up to ₹25,000 for purchasing health insurance plans for yourself, your spouse and your family. You must ensure that all insured parties, including you as the policy buyer, are under the age of 60 years to claim the deductions. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹50,000.

Besides paying the insurance premiums for your immediate family, you can also purchase a medical insurance plan for your parents and get an additional annual tax deduction of ₹25,000. Doing so enables you to obtain annual tax deductions of ₹50,000. Once again, all insured parties must be under 60 years for you to qualify for these deductions. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹75,000.

Besides paying the insurance premiums for your immediate family, you can also purchase a medical insurance plan for your parents and get an additional annual tax deduction of ₹25,000. Doing so enables you to obtain annual tax deductions of ₹50,000. Once again, all insured parties must be under 60 years for you to qualify for these deductions. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Deductions up to

₹1,00,000.

As the policy buyer, if you are above 60 years of age and still purchasing health insurance plans for your immediate family members (up to 60 years) and senior citizen parents, you can claim annual tax deductions of up to ₹100,000. The deduction is categorised as ₹50,000 for policies purchased for yourself and your kin and another ₹50,000 for policies purchased for your senior citizen parents. If your annual health insurance premiums cost less than the permitted deduction limits, you can also claim tax deductions for preventive health check-ups up to ₹5,000 per annum.

Other Tax benefits

Besides Section 80D, you can claim additional health insurance tax deductions under its sub-sections.

Step-wise Guide on Filing

Health Insurance Claim

The steps you must follow while filing a health insurance claim depend on whether you choose the cashless claim or reimbursement facility.

Steps to Follow for a Cashless Claim

1.

Intimation

Select a hospital from the insurer’s network.

2.

Approval/ Rejection

Inform the insurer about your chosen hospital..

3.

Hospitalisation

Present your health insurance card/policy at the hospital and seek admission.

4.

Insurance Liaison

The insurer’s representative contacts the hospital administration.

5.

Claim Settlement

The insurer takes care of the billing formalities and pays the bills up to the sum insured amount.

Intimation

Select a hospital from the insurer’s network.

Approval/ Rejection

Inform the insurer about your chosen hospital..

Hospitalisation

Present your health insurance card/policy at the hospital and seek admission.

Insurance Liaison

The insurer’s representative contacts the hospital administration.

Claim Settlement

The insurer takes care of the billing formalities and pays the bills up to the sum insured amount.

How to choose the

best plan for you?

How To Buy

Health Insurance Plans

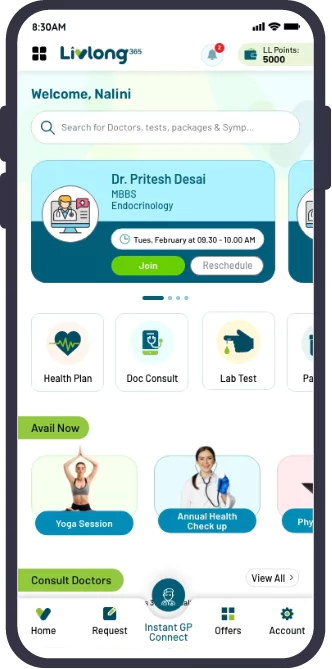

You can buy your medical insurance plan in several different ways. You may opt for the conventional route and purchase the policy through your insurance agent or broker. However, such intermediaries typically charge a commission for the services rendered. You can also visit the insurer’s offices and purchase your policy directly through them without paying intermediary fees. However, the most convenient way to buy a health insurance policy is online – through the insurer’s website.

1.

Research the various insurance companies online and check their claim settlement ratios.

2.

Research the various types of health insurance plans your chosen company offers and shortlist the plans you wish to buy.

3.

Read the terms and conditions, inclusions and exclusions, etc., about the chosen policies.

4.

Fill out the policy purchase form and provide details such as your name, age, gender, address, etc..

5.

Select your chosen policy and preferred sum insured amount, and add additional riders to the cart.

6.

Complete the payment process.

7.

The insurer will e-mail you your health insurance policy. You may also ask for a hard copy, which the insurer will send via post.

than Health Insurance?

FAQ'S

Join 2,00,000+ subscribers who get personalised health tips in their inbox

Buy Health Plan